Data Centers & Skilled Trades Careers: Powering the Future of Technology

Data Centers & Skilled Trades Careers: Powering the Future of Technology When you think of data centers, you might picture massive buildings filled with servers, blinking lights, and high-tech equipment. But behind every one of these facilities is a team of highly skilled tradespeople who

Trades Talk – March 2026

Apply for the Skills Lab Equipment Grant Program! Photo courtesy of Newark School of Architecture & Interior Design, a 2024-2025 Skills Lab recipient. Join Explore The Trades for a Skills Lab Webinar on Wednesday, March 11th from 2–2:30 PM CST. This session will give attendees

How to Avoid Student Loan Debt After High School | Explore The Trades

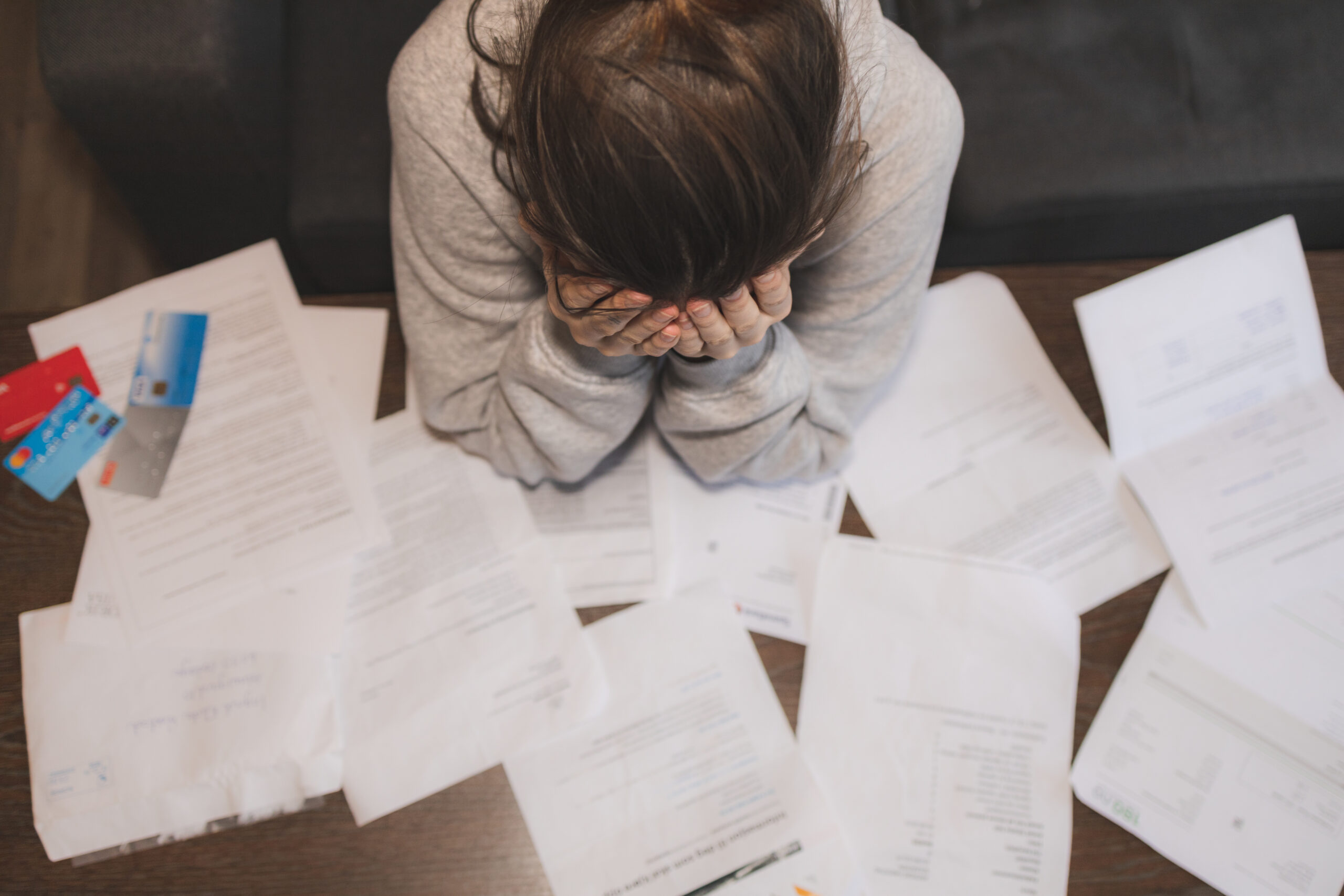

Learn how to avoid student loan debt after high school by exploring alternatives to college, trade school options, and careers that minimize student loans.

The Trades Discussion We Should Be Having

This blog post was originally written by Connor Williams of Ashton Mechanical Group published on February 6th, 2026 and is shared here with permission. I recently had the amazing opportunity to join other home services business owners on a fundraising trip to South Dakota in

Customer Service & Dispatch Careers in the Trades

Customer Service & Dispatch Careers in the Trades When people think about careers in the skilled trades, technicians carrying tools often come to mind. But behind every successful plumbing, HVAC, or electrical company is a team of customer service and dispatch professionals keeping operations on

Trades Talk – February 2026

Cast a Line for a Cause: Join Our 2026 Fishing Fundraiser! Get ready for an unforgettable experience at the Explore The Trades Fishing Fundraiser, taking place April 16–19, 2026, at Cajun Fishing Adventures in Buras, Louisiana. This all‑inclusive event offers two full days of guided

The College Enrollment Decline: Are Universities Losing Their Luster?

College enrollment has been declining for more than a decade. Explore enrollment trends in higher education and what shifting student choices mean for the future.

Trades Talk – January 2026

Celebrating Our 2025 Impact Explore The Trades is proud to share the highlights from our 2025 Impact Report. This year, we launched the fifth year of the “Explore The Trades Skills Lab, Built By Ferguson” equipment grant program and expanded our reach in school districts

Trades Talk – December 2025

Help Us Finish Strong! Explore The Trades is on a mission to connect kids, teens, and young adults with exciting careers in plumbing, HVAC, and electrical. Our free classroom poster kits (available in English, Spanish, and for kiddos ages five-11) make it easy to spark