Choosing what to do after high school is one of the biggest decisions a student will make. For many families, attending a four-year college feels like the default path. But with rising tuition costs and increasing student debt, more students and parents are asking an important question: how can you avoid student loan debt while still building a successful career?

Let’s take a look at the numbers and explore practical alternatives to college that can minimize financial stress and open doors to a rewarding future.

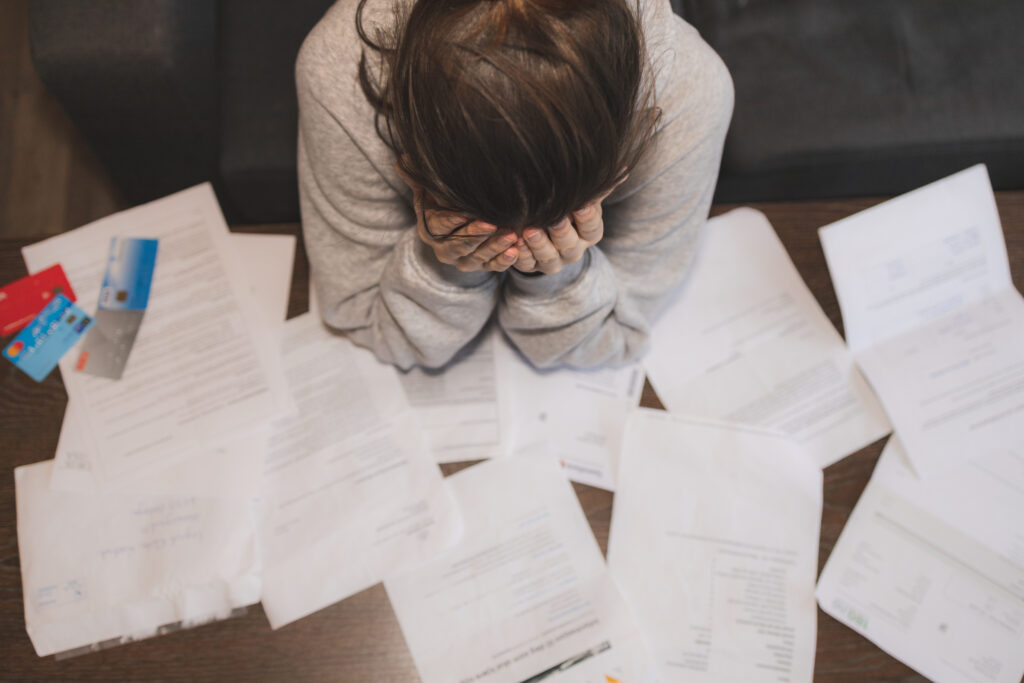

Understanding the current student debt landscape can help you make an informed decision:

For some college graduates entering high-paying fields, student loans may be manageable. However, for many others, repayment can delay major life milestones like buying a home, starting a family, or saving for retirement. Before committing to borrowing tens of thousands of dollars, it’s important to see if there is another path that aligns with your goals and financial future.

If your goal is to avoid student loan debt, or at least minimize it, consider these strategies:

Not all careers require a four-year college degree. Some industries prioritize hands-on experience, certifications, and apprenticeships over traditional academic pathways. Research salaries, job demand, and required training before selecting a major.

Trade school programs typically:

Many students complete technical training with little to no student debt.

Apprenticeship programs allow students to:

The time it takes to complete an apprenticeship is often similar to earning a bachelor’s degree. Instead of graduating with debt, apprentices often graduate with savings and experience.

Roxbury High School, a 2022-2023 Skills Lab Recipient School.

On-the-job training programs allow students to start earning immediately after high school. Instead of waiting four years to enter the workforce, many skilled trades professionals begin building income and career momentum right away.

Rising tuition may lead to long-term student debt, delayed full-time income, and competitive job markets in some fields. These factors don’t dismiss college as an option. But they do highlight the importance of choosing a path that aligns with your interests, financial goals, and long-term plans. If you’re wondering what your other options are after graduating, consider these:

These college alternatives can lead to stable, well-paying careers, particularly in essential industries like plumbing, HVAC, and electrical. Skilled trades careers are in high demand nationwide, resistant to outsourcing, essential to communities, and create strong pathways to business ownership. For students who enjoy hands-on work, problem solving, and tangible results, a trade career can be both financially and personally rewarding.

Bemidji High School, a 2023-2024 Skills Lab Recipient School.

If college is the right path for you, look for ways to reduce costs, such as starting at a community college, applying for scholarships, working part-time, or choosing a degree aligned with strong job demand. If you already have student loans, options like refinancing, income-driven repayment plans, or making extra payments toward principal may help you manage your debt more effectively.

Whether you’re a high school student, a parent, or an educator, understanding the available pathways is so important. At Explore The Trades, we provide free resources, career guidance, and tools to help students discover opportunities in the trades.

Before committing to years of student debt, take time to explore a future that works for you. Start by taking our quiz to see which trades career is right for you!